The national conversation around artificial intelligence is dominated by innovation. Quantum computing, data center expansion, processing power, storage capacity. The United States is the global leader in AI development, and that is not in dispute. But the conversation is focused on the wrong variable. The constraint on American AI dominance is not technology. It is power generation.

I have written about this before and the premise hasn’t changed. The future of American technology leadership will not be determined by the pace of innovation or the refinement of chip manufacturing. It will be determined by whether the national power grid can support the demand that these technologies require. That issue is more urgent today than when I first made the case. The timeline has compressed, the gap has widened, and the underlying infrastructure remains fundamentally inadequate.

The Grid Barely Supports What We Have Now

The American power grid, as currently constructed, barely generates enough capacity to sustain conventional requirements. This is not a future projection. It is an observable condition. Extreme winters stress the system to its limits. Hurricanes overwhelm it. When an electrical grid fails for any sustained period, the cascading effects on the affected population exceed the system’s ability to compensate. California imports a significant portion of its electricity from Arizona and Texas under normal operating conditions.

This is the baseline. The grid, as it exists today, cannot support even the meager near-term growth in AI technology and data center deployment, let alone what is projected over the next decade. And the demand curve is not linear. Each new generation of AI capability requires more processing power, more storage, and more energy to operate. The infrastructure required to support that trajectory does not yet exist, and it is not being built at the pace required.

The power problem will not be solved by solar panels or wind turbines. Those technologies are not effective primary tools for grid-scale power generation. They may contribute as a small component of a broader energy strategy, but they will not close the gap that exists between current grid capacity and what will be required by 2030.

The Infrastructure Investment That Did Not Deliver

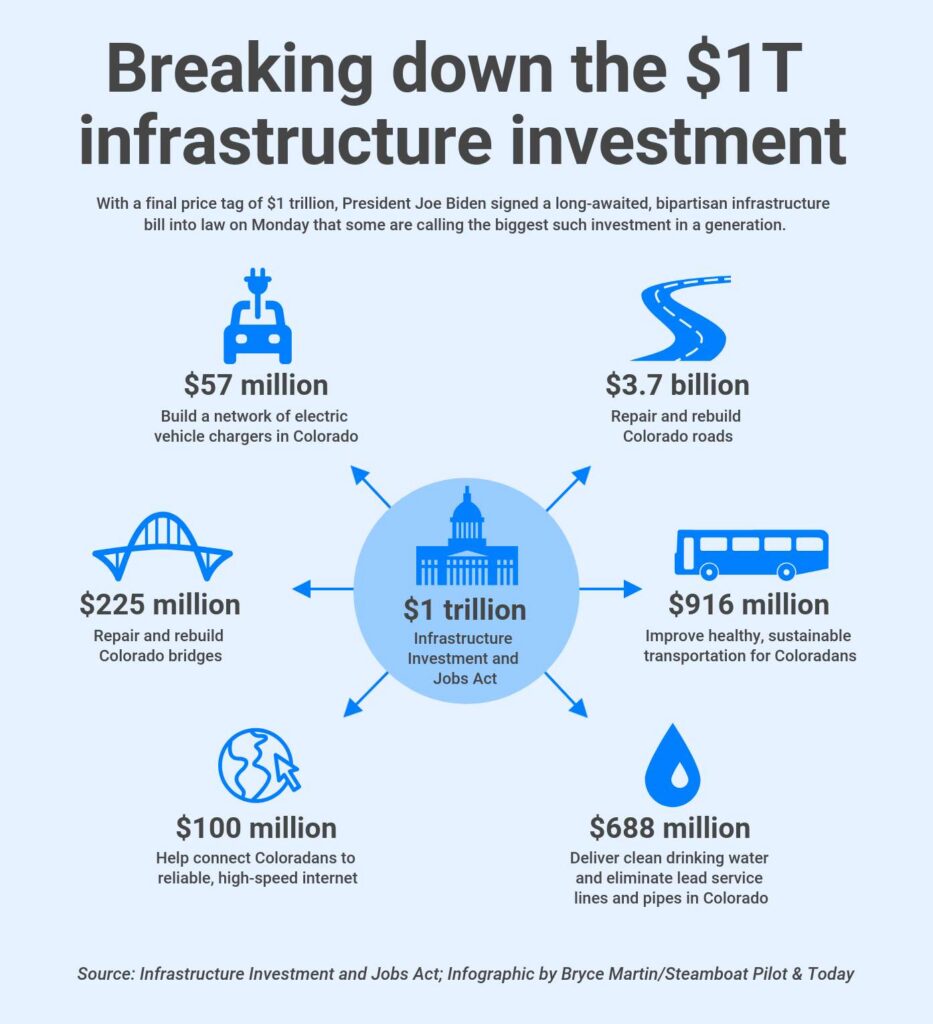

Under the Biden administration, Congress passed the $1.2 trillion infrastructure bill. The intent was sound. I was involved with several states in an advisory capacity, focused on how to direct infrastructure funding toward grid modernization, resiliency, redundancy, and expanded connectivity for schools, government, and private industry.

In too many cases, the money was directed toward problems with no measurable accountability. No tracking mechanisms. No performance benchmarks. Significant portions of the funding produced no demonstrable results.

In too many cases, the money was directed toward problems with no measurable accountability. No tracking mechanisms. No performance benchmarks. Significant portions of the funding produced no demonstrable results.

In partnership with i3solutions, we offered to build a website for one state that would have given every citizen full visibility into how their infrastructure money was being spent. Every project in the state, whether it was a road, a bridge, or an upgrade, would have been listed with the reasoning behind it, the company executing it, and the committed timeline. It would have shown whether a bridge that was supposed to be done in 36 months was actually on schedule. Or that a road was being widened because it serves as an emergency exit route so people are not trapped on an island during a weather event. All of it, right there for anyone to read.

The response was direct: the state did not want that level of transparency.

The point is not to relitigate the legislation. Not all of it was misused. But a substantial portion was not directed effectively, and the result is that the grid problem was not addressed. It remains unresolved, and it is worsening.

The Shortfall Is Already Measurable

The power deficit is not theoretical. It is appearing in current projections from the organizations responsible for managing the grid.

PJM Interconnection, the largest regional transmission organization in the United States, manages the power grid across 13 states serving approximately 65 million people. PJM is projecting a 6 gigawatt shortfall by 2027. That projection does not account for the most recently announced data center developments. As the gigawatt requirement rises over the next several years, the question becomes not only whether the grid can deliver what is needed, but whether the current capability can even sustain what is already being built. The answer, based on available data, is that it cannot.

The grid is not a single uniform system with a single fix. Some regional grids require efficiency improvements. Others require fundamentally better power supply. And many need to be rebuilt entirely. The data centers currently under construction are already creating measurable strain on regional capacity, and the next wave of announced facilities has not yet been factored into baseline projections.

There are also secondary constraints  that compound the infrastructure challenge. TSMC, which manufactures the chips these systems depend on, is at maximum production capacity with orders committed through 2029. Even if the power problem were resolved today, chip supply constraints would continue to limit the pace of data center deployment. The demand pressure will also drive up costs across the broader technology sector. Consumer hardware, including personal computers, will increase in price as chips become scarcer and supply-demand dynamics tighten further. The chip shortage and the power shortage are parallel constraints, and neither is being resolved at the pace the market requires.

that compound the infrastructure challenge. TSMC, which manufactures the chips these systems depend on, is at maximum production capacity with orders committed through 2029. Even if the power problem were resolved today, chip supply constraints would continue to limit the pace of data center deployment. The demand pressure will also drive up costs across the broader technology sector. Consumer hardware, including personal computers, will increase in price as chips become scarcer and supply-demand dynamics tighten further. The chip shortage and the power shortage are parallel constraints, and neither is being resolved at the pace the market requires.

Compounding the power shortfall is a workforce shortfall. The United States does not have enough electricians, welders, and systems integrators to build this infrastructure at the required pace. The skilled trades workforce has contracted in precisely the areas where demand is accelerating most rapidly. I have heard this from at least three senior technology company leaders, including the head of Nvidia. They all made the same observation: the next generation of high-demand, high-value careers will not be in software. They will be in the trades that physically build and integrate data center infrastructure. That assessment is not speculative. It reflects the reality that the people who build these systems will matter as much as the people who design them.

Based on direct conversations with power companies, I believe current projections represent the low end of actual demand. The real requirement curve is steeper than what is being planned for, and the gap between planning assumptions and operational reality will widen if projections are not revised upward.

A Security Vulnerability Embedded in the Grid

There is an additional dimension to the grid problem that receives insufficient attention. In 2019, the United States determined that China was selling large-scale transformers containing backdoor code that did not meet established cyber security standards. Federal policy at the time prohibited the installation of these components in the American grid.

![]() On January 20, 2021, that prohibition was reversed. The United States currently has several hundred Chinese-manufactured large transformers embedded in its power grid, each representing a known cyber vulnerability.

On January 20, 2021, that prohibition was reversed. The United States currently has several hundred Chinese-manufactured large transformers embedded in its power grid, each representing a known cyber vulnerability.

This is not a speculative risk. These are components manufactured by a strategic competitor, installed in critical national infrastructure, with documented security deficiencies. I addressed this vulnerability and the broader grid security landscape in greater detail in my MIDLIFE Infrastructure analysis.

The Strategic Implications for Great Power Competition

The United States leads the world in AI innovation. That position is not in question. What is in question is whether the United States can sustain that lead, because sustained technological dominance requires sustained infrastructure capacity, and that is where the competitive picture shifts.

China faces none of the constraints  that are slowing American power infrastructure development. China commissions new coal-fired power plants on a near-monthly basis. Its energy supply chain includes pipeline oil from Russia, discounted crude from Iran (China purchases approximately 90 percent of Iran’s oil output), and until recently, below-market oil from Venezuela. Those discounted sources are now under pressure, and China’s energy costs may increase as a result. But the fundamental asymmetry remains: China is willing to expand power generation capacity by any means available, at whatever pace is required, without the regulatory, environmental, or political constraints that affect the pace of expansion in the United States.

that are slowing American power infrastructure development. China commissions new coal-fired power plants on a near-monthly basis. Its energy supply chain includes pipeline oil from Russia, discounted crude from Iran (China purchases approximately 90 percent of Iran’s oil output), and until recently, below-market oil from Venezuela. Those discounted sources are now under pressure, and China’s energy costs may increase as a result. But the fundamental asymmetry remains: China is willing to expand power generation capacity by any means available, at whatever pace is required, without the regulatory, environmental, or political constraints that affect the pace of expansion in the United States.

That asymmetry is strategic, not technological. If the United States is constrained by grid capacity, workforce shortages, chip production limitations, and the inability to build power infrastructure at the necessary pace, then the innovation advantage becomes irrelevant. Maintaining technological leadership is not solely a function of research and development. It is a function of the national will and infrastructure required to operationalize that research at scale.

What Must Happen

None of these problems are irreversible. But the window for action is narrowing, and the pace of response must match the pace of demand.

Deregulation must continue and accelerate. The current policy direction, enabling companies such as Meta, xAI, and others to construct data centers with dedicated, independent power generation, is correct. These facilities must be encouraged and they must be built to the right standards. Any data center that remains connected to a municipal grid creates two problems: it reduces the power available to the civilian population, and it introduces a cyber security exposure that operates in both directions. Data center power infrastructure must be self-contained.

Deregulation must continue and accelerate. The current policy direction, enabling companies such as Meta, xAI, and others to construct data centers with dedicated, independent power generation, is correct. These facilities must be encouraged and they must be built to the right standards. Any data center that remains connected to a municipal grid creates two problems: it reduces the power available to the civilian population, and it introduces a cyber security exposure that operates in both directions. Data center power infrastructure must be self-contained.

The national energy strategy must be multi-source. Small modular reactors, from companies such as NuScale and Oklo, will be essential. Liquid natural gas and fossil fuel sources, including coal and oil, must be part of the equation. Companies like Constellation, PJM, and Siemens will play a role in integrating the physical infrastructure. IT integration specialists, including i3solutions, will be needed to provide the technical expertise and advisement required to bring hardware, software, and operational systems together inside these environments. Dedicated fuel sources must be located at or directly connected to the facilities they serve.

The compromised Chinese-manufactured transformers currently in the grid must be identified and removed. The vulnerability was recognized in 2019, the protective policy was reversed in 2021, and several hundred compromised components remain in the system. That condition is unacceptable and must be remediated.

Projection models must be revised upward. From direct engagement with power companies, it is clear that current planning assumptions understate actual demand. The planning must be calibrated to the real trajectory, not to conservative estimates that will be overtaken by events.

The Bottom Line

The United States possesses every advantage in AI innovation. Translating that advantage into sustained dominance requires the infrastructure, the energy capacity, and the national will to support it. This is not an abstract policy discussion. It affects every organization that depends on AI processing capability, from the Department of Defense to the intelligence community to private sector firms operating in classified environments. The demand for AI processing will increase across all of these sectors over the next five years. The question is whether the power infrastructure will be there to support it. The technology is not the limiting factor. The power is.

i3CA combines strategic geopolitical expertise with operational advisory support for organizations navigating Great Power Competition, infrastructure resilience, and national security technology challenges.

If your organization is working through power infrastructure planning, grid resilience, or the intersection of energy security and technology strategy, request a mission-specific briefing at tony.thacker@i3solutions.com.

No comments yet

Be the first to leave a comment!